Reflections of 2025, year end review and 2026 goal setting

As I sit drinking coffee on the edge of a stream on 01 January 2026, I reflect over the last year. I feel extremely grateful for this trip that I am on (thank you Jen and Jonathan), getting to stay in a cabin on the edge of a stream, just 500 metres away from the sea. I only just realised that this trip was one of the goals I set myself last year.

Side note: I do think in 2026 we should just have the internet all the time if we want! What is up with camping still being associated with crappy internet? Well, perhaps because degenerates like me get forced to be present and disconnect (at least partially) for a moment.

Anyway, I have this ritual that I have been doing for the last 7 or 8 years and forcing my household to do also: this process of goal setting that I call 12, 12, 12, where on New Year's Day we set our annual goals and then set milestones along the way to help us achieve our larger goals. We do this for the business also, and my goals are often connected to the business.

I have all the previous years' 12, 12, 12s in notebooks that I have written over the years, which is awesome. At this time of year, I may look back and see what I was writing, thinking and dreaming years ago. It is a wonderful way to see how far you have come and to see where you are still aligned with the past you and therefore where your thinking may have changed. It is always good to go back to the last year, and here I have my goals for last year…

- End the year, sleeping in a cabin, no drama, able to take holiday without worry - Complete

- Maintain and improve connection with everything in the family - Complete

- Find new home and settle in - Complete

- Maddition cash flow positive - Missed

- Make 750k in revenue - Missed

- Compete in Jiu Jitsu - Missed

I have never managed to hit all my targets for a 12-month time frame. The framework is approached with the same principles as OKRs, which is heavily incorporated in the Google ways of working, and they seem to have it together—after all, I do think they are the best business on planet earth.

If you want to read my full article on how I use 12,12,12 goal setting.

2025: A Year of Growth and Challenges

Anyway, so 2025…what a year it has been. I think that in many regards this year has been my favourite year. Despite the challenges, there have been several occasions throughout the year that were extremely difficult…including the end of the year which in many instances felt like a long string of unfortunate events.

It has been a wonderful experience seeing our team and people close to me growing and getting rewarded for their hard work. I am inspired by all of you. And a continued appreciation for the stakeholders and shareholders of eccuity, new and old!

Be True to Thy Known Self

Sometimes everything you do goes right and then there are other times that the outcomes are not what you desired.

I think however, as my beard starts to show a few greys, my hair starts to thin and the young whippersnappers at Jiu-Jitsu continue to try and kill me, I become a little more philosophical about life and believe more deeply that the principles and frameworks we adopt in our everyday life become an ever-increasing contributor to success.

Last summer I put together 10 rules that I use to help myself from getting into trouble in all areas of my existence. In fact, I am in the middle of writing a book currently titled: Die Empty, Live Full - How to get whatever you want in 5 years.

After that work I did on myself last year especially and into this year, I am coming to the conclusion that for us to really get the best out of ourselves in life, we need to live by our own values and what we want, rather than bending to what we think we should want or what the world is trying to mould us into.

And as business owners that directly contributes to the businesses we build and how they operate.

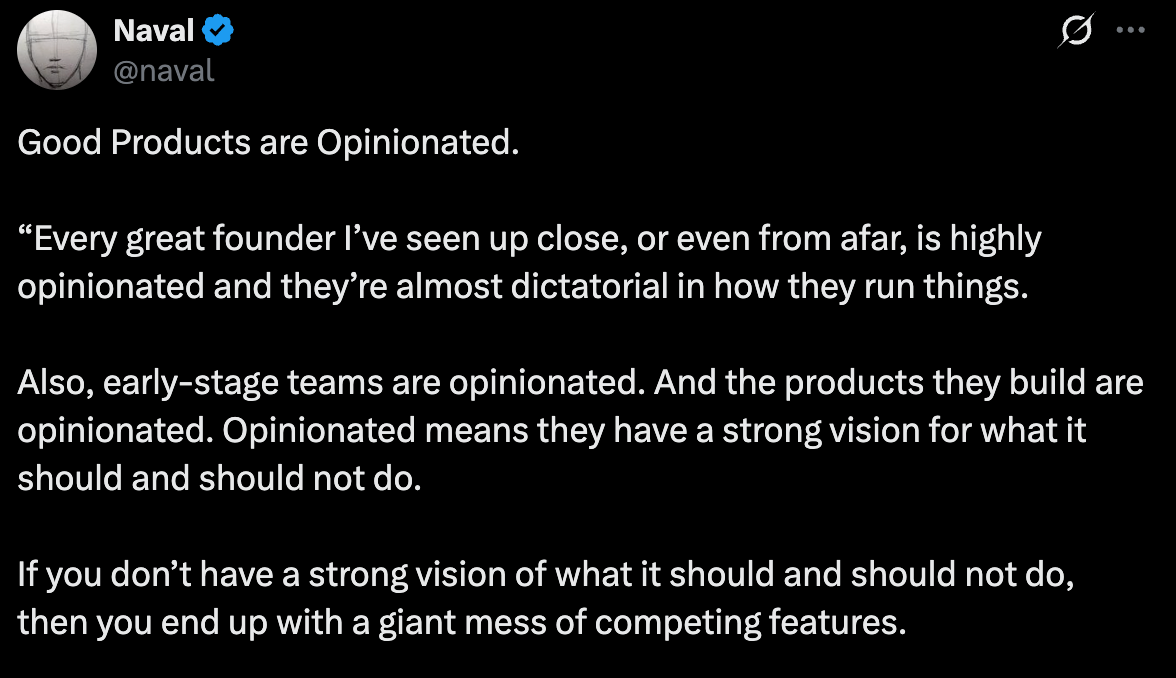

Naval Ravikant had some great posts on X quite recently which really hit home for me on a personal note and made an observation that I agree with in this evolving landscape of business: that if we want to stand up in this new world, our products need to be opinionated. The days of sitting on the fence are past us.

Sometimes you are too nice, too accommodating, letting it slide and too idealistic… you risk getting taken advantage of. The key I guess is to keep turning up, stick to your values and focus on actions not words. It is easy to postulate intelligence by regurgitating information or playing games politically to gain short-term influence, but very few take real action.

That is any individual operator's biggest advantage: taking action. Today.

eccuity

We started the year with a bunch of goals we wanted to achieve on the product roadmap side and we have really improved the platform and been honing our offering for the memberships all year and building up our brand in the market.

Since we started doing podcasts we have recorded approximately 200 so far, participated in a number of fun industry events and picked up some nice earned media!

I am glad that we have ended the year as a company that is offering the highest quality mechanism for transacting in US equities, ETFs and Crypto with a very competitive interest rate paid to our customers who use our sweep programme.

With the addition of our memberships and net worth tracker released we now can assist in tracking across a user's entire portfolio irrespective of the asset class. This is extremely well suited to the New Zealand high net worth community given the extraordinary allocation to illiquid assets. By also focusing our offer on insights and guidance, leaning into our vision that "We believe everyone should have the right to build wealth for themselves and have the freedom to choose how they get there". With such a large proportion of the New Zealand economy running on SMEs and sole traders, it is essential that there are ways to help people get to answers that are nuanced, not connected to the consumption of a financial product but absolutely impact the eventual financial success of an individual, household or family office (estate).

My reflection so far on how that is going is that frankly we still don't do a good job of explaining what we do and how we do it and I generally think we need to massively up our game from an onboarding perspective.

I am currently going through and completing the appropriate courses to allow us to keep pushing the depth and value of what we can offer and we do have designs for a very interesting Kiwisaver product that will be a very strong offering in a market that I think has a long way to go in order to deliver comparable product value that we see available in more developed markets.

After all, if we are all going to index towards the S&P 500 (not that I think that is an overly sensible idea), let's all blindly use the Vanguard ETF. After all, its cost is negligible and there is no need to have 5 or 6 players doing variations of the same thing and charging between 5-20x what the international markets can charge. Seems like easy money and the market gets it, but just not overly stimulating for the mind and perhaps there are inherent concerns about being overly indexed to the S&P 500. The market is not just the S&P 500, especially with market cap weighting dynamics. But hey, it's been a treat!

Perhaps I am contrarian to my detriment, however, if we do create anything in that space it will at the very least be differentiated.

Kiwisaver and the Increased Contribution

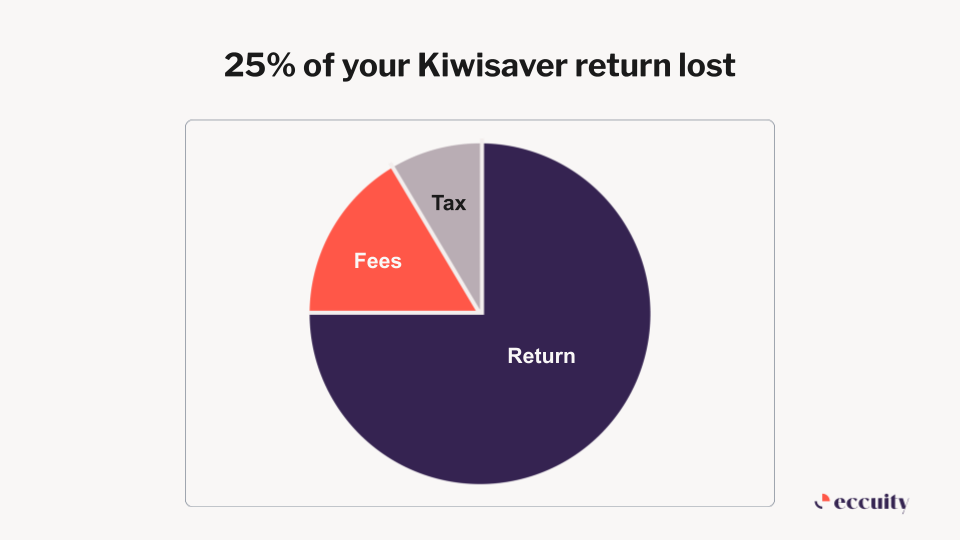

Should Kiwisaver Savers Pay 25 cents of Every Dollar Earned from Saving?

I have a few problems with this. But I will be a good lad and start off with something positive.

First off, I think that households should be aiming to save more than 12% of their annual income, especially if they are not in a form of employment where they are generating equity appreciation from the activities they are doing.

So this could be business owners, founders, those who earn equity for milestone-based outcomes etc. In that case, I do think you can be a little less harsh on yourself because the time you spend on your work is building equity. Typically in New Zealand, most of an individual's wealth would come from their business.

Two key percentages that highly resonate with me and naturally put people in an advantageous spot would be to save 20-30% of their after-tax income and have the cost of their shelter (rent or mortgage) be no more than 25% of your household income. Now we know that both of these are not happening unfortunately.

Now onto the issues I have with this celebration of an increase to a 12% contribution as a standard.

Firstly, I just have fundamental discomfort with the idea that the largest portion of savings the average individual will be able to save is forced into a regime where the only way they can get out is the following:

- First home purchase

- Retirement - 65

- Financial hardship

Some may not like it, but I have inherited too much of Charlie Munger's teachings to not have a strong streak of conservatism in me which is prone to questioning government-run initiatives.

Suppose I can get over the fact that we think it's a good idea to impose people into a construct that keeps the client's capital in the Kiwisaver regime with the 3 above choices. I do think it would be interesting to stress test our thinking around the conditions that people can access the capital or at the very least make the cost to be in the regime at all palatable for individuals—that it's their money. Ninety percent of it shouldn't continuously be taxed by the government and funds management industry after they already got taxed earning it. It makes little sense to me.

So the first question I have is of course…where is the tax incentive for the saver? If they are going to lock your savings regime for 30-45 years, then the least you can give that saver is to be reasonable with the tax considering they are living in a cost of living crisis and being taxed multiple times over on money they earned years ago.

And as previously mentioned, the costs in the funds management are still high overall and I look forward to competitive pressures encouraging firms to improve margins and then deliver them to their clients and to innovate to give savers a more dynamic universe to operate in.

On an aggregate basis, look at the cost to savers for being in Kiwisaver. What is the appropriate cost that savers should incur?

With clear changes in demographics and at the same time we have a very fluid time ahead of us with the shape of employment, we need to be stress testing our assumptions when it comes to how we help our local society maintain or improve our standing in quality of life and have skin in the game when it comes to backing NZ Inc.

Do More, Our New Normal

With the advent of AI and how quickly we are all attempting to adopt it and shoehorn AI into our workflows, we are seeing improvements and potential which is creating a feedback loop. From a psychological perspective that I have picked up over the last year interviewing over 100 business owners on the podcast and from our portfolio, the pressure to do more and go faster has never been so prominent.

I will go into more detail on AI and DIY development below. My gut is telling me that speed is great, but now with speed increasing, precision is becoming more important.

Less is more.

Technology and Consulting Landscape

There has been a narrative growing in the software space, specifically enterprise SaaS, which has definitely put pressure on the valuations of certain software companies and consulting where the market is speculating that AI will disrupt their businesses.

Enterprise SaaS Performance in 2025: The enterprise SaaS sector saw continued maturation in 2025, with median growth rates at 26%, down from previous years' higher levels. Companies have been cutting expenses across the board to maintain profitability, with particular focus on sales and marketing efficiency. The global SaaS market is projected to reach $300 billion in 2025, with AI adoption being a major driver—76% of SaaS companies are now using or exploring AI for operations.

Consulting Industry in 2025: The consulting industry demonstrated resilience despite economic headwinds. Global consulting revenues are expected to reach $1.06 trillion in 2025 and $1.32 trillion by 2029. Strategy consulting specifically is expanding rapidly, projected to reach $91.38 billion by 2025, representing a 9.9% CAGR since 2018. However, the industry faces challenges as firms must navigate between traditional advisory models and AI-driven disruption. Digital transformation consulting is the bright spot, expanding at 28.5% CAGR as businesses adopt AI, automation, and cloud technologies.

AI, Automation and DIY Development

There is no doubt in my mind that AI can solve issues in businesses, taking out large cost components and improving operational efficiencies…this is the low-hanging fruit stuff, not science or technological breakthroughs.

Internally we have seen incredible operational improvements and a general increase in productivity of the team, especially those in the team that have taken to the technology faster.

It is now possible to get a working MVP up and running in weeks now. Something that may have previously taken a couple of months to deliver.

And the skill gap to get that working thing going has never been lower. Now, the issues are in getting those MVPs to production. Currently the technology and non-technical users struggle to validate the quality of what they are putting together and asses potential security issues, considering the appropriate safeguarding through data integrity and backup protocols etc.

My advice would be to use it and embrace it in workstreams where you have a path and know that you are going to make use of the code/automation. Most software never gets deployed and from what I am seeing that percentage isn't going to meaningfully change even though there has been a clear democratization of technical capability/intelligence across all of humanity with the advent of LLMs.

What About Web3, Crypto and Stables

So this year I have been making a conscious effort to improve my understanding of the blockchain space at large!

I started the year begrudgingly asking myself some tough questions about my aversion to embracing the space. So I got to work, reading, learning, speaking to smart people in the space and where the adoption is, and where the garbage is.

So here is what I have learned:

Participating in a well-known network's DeFi builder program was an experience. Honestly, overall it seemed that behind the scenes there was an undercurrent of stress and misalignment with the overall ecosystem which was clear.

Much of the dynamics of the incentives that platforms try to give their users feels a little backwards to be honest. If a product is good and solves a problem, you don't need to give anything other than that value to the user.

There is a use case for blockchain in the probate space which is where we are working on, however, most of the industry seems more focused on speculation and gambling-like dynamics. Look at how Polymarket has succeeded.

From the events and blockchain engagements this year, I wish I could write this memo saying that I am more convinced and therefore bullish. However, I probably have a lot more questions than I started the year with.

I think the repackaging of old products that already exist through tokenization seems interesting, but again, in some cases it's like…why? We have a bunch of suitable solutions.

Clearly the big winner in the blockchain space has been the stablecoin space where there has been incredible adoption and the use case makes sense, especially with the scale and improved liquidity. Then the cynic in me feels like it's the U.S. way of making a bunch of retail hold the bag on their treasury bonds.

I think there are lots of insiders that profiteer from the ecosystems and are getting a disproportionate upside and that there is a clear trend towards more centralization. The technology will likely be adopted and eaten by the banks and big financial institutions or directly by governments and central banks as a way to curcumvent the banks, disrupting their power.

In terms of Bitcoin, well most of my rationale for someone owning it is a distrust of the current monetary system and having a bet that perhaps Bitcoin gets it done. But I dunno…still more questions. I could sleep better at night owning Google rather than Bitcoin. Dynamics change, my mind changes and my conviction in the asset class currently sits at about 5% of a portfolio.

Asset Prices and Speculation

OpenAI Funding Round

Current Fundraising Status

OpenAI is in preliminary discussions to raise up to $100 billion in a new funding round that could value the company at $750-830 billion. The company aims to close this round by the end of Q1 2026 (March 2026).

Key Valuation Metrics

- Current valuation: $500 billion (as of October 2025 secondary transaction)

- Proposed new valuation: $750-830 billion (depending on final terms)

- Valuation jump: 50-66% increase from the October 2025 valuation

In March 2025, OpenAI closed what became the largest private technology financing in history—a $40 billion funding round at a $300 billion post-money valuation. The round was led by SoftBank, contributing $30 billion, with participation from Microsoft, Coatue, Altimeter, and Thrive. OpenAI will initially receive $10 billion with the remaining $30 billion by the end of 2025, though funding may be reduced by up to $10 billion if the company fails to convert to a for-profit entity by December 31, 2025.

Approximately $18 billion of this funding is earmarked for OpenAI's Stargate infrastructure project. At the time of the funding announcement, ChatGPT had reached 500 million weekly users, up from 400 million just a month prior. The company's annual recurring revenue has surged from $10 billion in June to an expected $20 billion by year-end.

By August 2025, OpenAI had raised an additional $8.3 billion, bringing in new investors including private equity giants Blackstone and TPG, with Dragoneer Investment Group committing an impressive $2.8 billion—one of the largest single checks ever written by a venture capital firm.

My conclusion is that if there was an AI bubble, lots of powerful institutions would be desperate to get companies like OpenAI, SpaceX, Stripe and Anduril public while the music is still playing. No doubt many insiders and early investors have filled their boots in these assets and liquidated large portions along the way as well as employees.

Silver Performance in 2025

Silver had an extraordinary year in 2025, surging approximately 120% and breaking all-time records. The white metal broke past $65 per ounce for the first time ever in December, capping its best performance in decades. By late December, silver was trading above $72 per ounce.

This rally stems from a powerful convergence of factors. Industrial demand from solar, EVs, and AI data centers is soaring while the market faces its fifth consecutive year of supply deficits. Bank of America raised its 12-month target to $65, while BNP Paribas sees potential for $100 by late 2026. Mine production remains stagnant and physical shortages persist in London.

The surge goes beyond Fed easing. U.S. fiscal deficits are ballooning, geopolitical tensions from Ukraine to trade wars are escalating, and the investor base is broadening—stablecoin issuer Tether and Asian pension funds are buying in. Central banks continue diversifying away from dollar-denominated assets, providing a price floor even when investor positioning gets crowded.

I am seeing an influx of watch and jewellery flippers go big on social media and get far too rich. When I see this behaviour on social media, I get skeptical. The prevailing narrative can be true at the same time as it being true that an asset is in a speculative frenzy. Whenever we are baking in the future we are by definition speculating.

Equities Performance in 2025

The S&P 500 delivered solid returns in 2025, posting approximately 17.9% total return (including dividends) for the year. Through September, the index showed a 12.0% price return with an additional 1.0% from dividends, for a total return of 13.0% year-to-date. This marks the third consecutive year of double-digit returns following 25% in 2024 and 26.3% in 2023.

Importantly, over half of the S&P 500's return in 2025 came from profit growth, not just multiple expansion. Forward 12-month earnings per share rose to $292, up 7.4% year-to-date. Breaking down the 13.0% YTD return through September: 7.6% came from earnings growth, 4.4% from multiple expansion, and 1.0% from dividends—meaning about 66% of returns came from actual profits.

Margin expansion was a key driver, with forward profit margins reaching a record high of 14.0%. Sales growth contributed 5.2%, margin expansion added 2.4%, multiple growth 4.4%, and dividends 1.0%. The market remained near all-time highs throu\gh year-end, trading around 6,900 points on the final trading day.

Conversely to strong performance of many liquid assets, we live in a K-shaped economy where low-end consumers and illiquid assets like private equity, private credit and real estate have struggled. That to me is a bit of a signal to the underlying strength of the economy and monetary system.

Inflation Never Left the Building

Global Inflation Picture: Year-on-year inflation in the OECD remained elevated through 2025, hovering between 4.0% and 4.2% from March through July. As of July 2025, OECD inflation stood at 4.1%, with core inflation (excluding food and energy) at 4.4%. Energy inflation turned slightly positive at 0.3% after being negative earlier in the year, while food inflation remained stable around 4.5%.

In the G7, inflation remained at 2.6% in July, with core inflation at 3.0%. The euro area saw inflation stabilize at 2.0% in July, with services inflation at 3.1%. In the U.S., the Consumer Price Index rose 2.7% year-over-year in July, with core CPI climbing to 3.1%—the highest since February and up from 2.9% in June. Economists project core inflation will escalate to 3.8% by year-end as tariffs have a more substantial impact on consumer prices.

New Zealand Inflation: New Zealand's annual inflation stood at 3.0% in the September 2025 quarter. This was a significant improvement from the peak of 7.3% in 2022, bringing inflation back within the RBNZ's 1-3% target band for the first time in three years. This allowed the RBNZ to pivot and deliver 125bp of cuts from August 2024, with expectations of a further 125bp of cuts by Q3 2025, taking the cash rate to 3.00%.

The challenge with government shutdowns impacting transparency on true inflation is that we rely heavily on Stats NZ data releases, and any gaps in reporting create uncertainty around the accuracy of inflation measures. While headline numbers have improved, many New Zealanders continue to experience persistent cost pressures in essentials like food, housing, and services.

We are still dealing with and experiencing unprecedented inflationary pressures. With costs continuously going up, price shocks and asset speculation at high levels, it is clear that regardless of the headline number dropping, we have seen persistent and understated data from central providers. When I look at the market and compare it to history, I keep getting the urge to get long dated treasuries. What keeps holding me back is that there is no part of me that thinks the yield on those treasuries makes any sense given the level of underlying inflation and fiscal irresponsibility going on.

Interesting Themes for 2026

I think it a great benefit to try to truly understand what is going on in the market in real-time. The task of learning and reading on current events can be of great benefit to you personally and your career.

Trying to profit from that leaves you open up to being wrong and looking silly. So bear that in mind if you too try to gain a market view.

Energy

Global energy demand continues to accelerate driven by AI data centers, electric vehicle charging infrastructure, and general economic growth. The energy transition creates both traditional and renewable energy opportunities. With geopolitical tensions elevated and supply constraints in certain regions, energy infrastructure and production companies remain well-positioned.

Technology

While AI continues to drive excitement and investment, valuations in the technology sector are stretched. Enterprise SaaS companies face margin pressure and slowing growth rates. The sector requires careful selectivity rather than broad exposure. Companies that can demonstrate real AI integration and productivity gains will outperform those simply rebranding existing products.

Bonds

With central banks in cutting cycles and recession risks elevated, long-dated treasuries could perform well. The RBNZ has already delivered 125bp of cuts with more expected. However, fiscal irresponsibility and persistent inflation make the risk-reward less compelling than historical precedents would suggest. The disconnect between yields and true inflation remains a concern.

Healthcare

An aging demographic, continued innovation in treatments and diagnostics, and stable demand characteristics make healthcare attractive. The sector tends to be less correlated with economic cycles. Medical technology, biotech innovation, and healthcare services providers offer diversified exposure to this secular growth trend.

Beaten Down Consumer Brands

Companies like Lululemon (LULU) and Nike (NKE) have been destroyed over the last period. LULU dropped 52% in 2025, making it the fourth-worst stock in the S&P 500. Nike's revenue declined approximately 10% to $46.31 billion, with earnings down 43.5%. Both trade at historically low valuations—LULU at just 11.5x earnings (lowest in over ten years) and Nike showing signs of turnaround under new CEO Elliott Hill. There may be value here if these companies can execute on their turnaround plans, but timing is critical. Brand strength and distribution advantages haven't disappeared—execution has faltered.

Acquisitions and Special Situations

With the current U.S. political regime, M&A activity will likely accelerate. Special situations and arbitrage opportunities should be plentiful for those with the expertise to evaluate them properly. Private equity continues to sit on record dry powder, and strategic acquirers are hunting for bolt-on acquisitions and market consolidation opportunities.

Precious Metals

Precious metals are garnering high interest and speculation due to the dollar devaluation narrative. With central banks continuing to diversify reserves and geopolitical tensions elevated, gold and silver provide portfolio insurance. However, after silver's 120% run, near-term returns may be muted. The fundamental case remains intact—supply deficits, industrial demand, and monetary concerns—but entry points matter significantly after such a dramatic move.

Foreign Exchange

Currency markets will likely be extremely volatile given diverging monetary policies, trade tensions, and geopolitical uncertainty. This creates both risks and opportunities for those positioned correctly. The U.S. dollar's dominance faces challenges from BRICS alternatives and central bank diversification, while emerging market currencies face their own inflation and political pressures.

New Zealand Economy

New Zealand's economy showed resilience in 2025 after a challenging period. After a particularly tough year in 2024—with GDP estimated to have fallen by 0.5%—the economy expanded 1.1% in Q3 2025, rebounding from a 1.0% contraction in Q2. This beat forecasts of 0.9% growth and marked a return to expansion after back-to-back contractions.

Business services rose 1.6% and made the largest upward contribution to growth, driven by a 2.1% rise in professional, scientific, and technical services. The annual GDP growth rate stood at 1.3% in Q3 2025. However, the full-year outlook has been revised down, with GDP growth now expected around 1.2% for 2025 compared to earlier expectations of 2.4%.

The unemployment rate peaked at 5.4% in the first half of 2025 before easing over the rest of the forecast period. Lower interest rates following the RBNZ's 125bp of cuts since August 2024 are supporting increased household and business activity. Business and consumer surveys have improved, card spending figures have risen, and the housing market appears to be stabilizing as mortgage lending has increased.

Looking ahead, GDP growth is forecast to pick up to 1.8% in 2025 (from a low base) and accelerate to 2.9% in 2025/26 and 3.0% in 2026/27. The government's new Investment Boost policy is expected to increase real GDP by up to 0.4% within the forecast period.

It is clear that our economy has a lot of potential and given its relatively decentralized nature (outside of core financial services and housing), we have an incredible amount of potential. Given the ever-decreasing cost of taking an idea from 0 to 1 with AI, automation, the internet and robotics, smaller human populations can thrive.

We are thrilled to be partnered with Boston ME, which is a division within Australian institution Boston Global, to bring more liquidity and funding to New Zealand private businesses and startups.

We just got accepted as a part of the acceptable investments governed by Invest NZ.

New Zealand is a really interesting opportunity, both as an economic and geographic safe haven but also as a place where investors can find returns.

In our 2025 Business Sales Report, we concluded that many New Zealand businesses could be more profitable, productive and valuable if more were able to modernize, do technological transformations and de-risk key persons within their businesses—these business valuation multiples could expand.

The same goes for startups in the region. On average our valuations in the startup space are much lower than the U.S. (for good reason too).

We believe this fund has a great opportunity to help real businesses in New Zealand thrive.

The Holy Grail of Investing

Ray Dalio, founder of Bridgewater Associates (the world's largest hedge fund), has long advocated for what he calls the "Holy Grail" of investing: finding 15-20 good, uncorrelated return streams.

Dalio's research demonstrates that diversification is not about owning many things—it's about owning uncorrelated things. If you can find 15 to 20 good, uncorrelated return streams, you can reduce your portfolio risk by 80% without sacrificing expected return. With 20 uncorrelated assets, the chance of losing money each year drops to only 12%.

The concept is grounded in Modern Portfolio Theory: as the number of uncorrelated assets in a portfolio increases, the portfolio's standard deviation (risk) decreases dramatically. When assets have 0% correlation, the risk reduction is most dramatic—with about 15-20 such assets, portfolio risk approaches the lowest possible level. Even with 10-40% correlation, significant risk reduction occurs, though the benefit diminishes as correlations rise.

Dalio emphasizes investing across various asset classes (equities, bonds, commodities), sectors, and geographic regions to balance risk and reward. Examples include:

- Equities: High potential returns, spread across sectors and regions for low correlation

- Bonds: Stability and safety, with long-duration treasuries acting as a cushion

- Commodities: Uncorrelated assets like gold that stabilize during market fluctuations

- Real estate: Both direct ownership and REITs

- Alternative investments: Private equity, hedge funds, litigation finance

- Geographic diversification: Exposure to different economic regions and currencies

In conclusion, I think that 15 streams is impractical for most market participants, and even if you get quite wealthy…let's say $2,500,000 USD (approximately $5m NZD) net worth, then you are still likely to only have 3 or 4 meaningful streams of income/equity…and that is, if relatively evenly distributed, a more realistic and achievable goal. Sometimes the billionaire who runs one of the largest hedge funds in the world may not have the answer for the everyday individual saver and market participant trying to earn a loaf of bread.

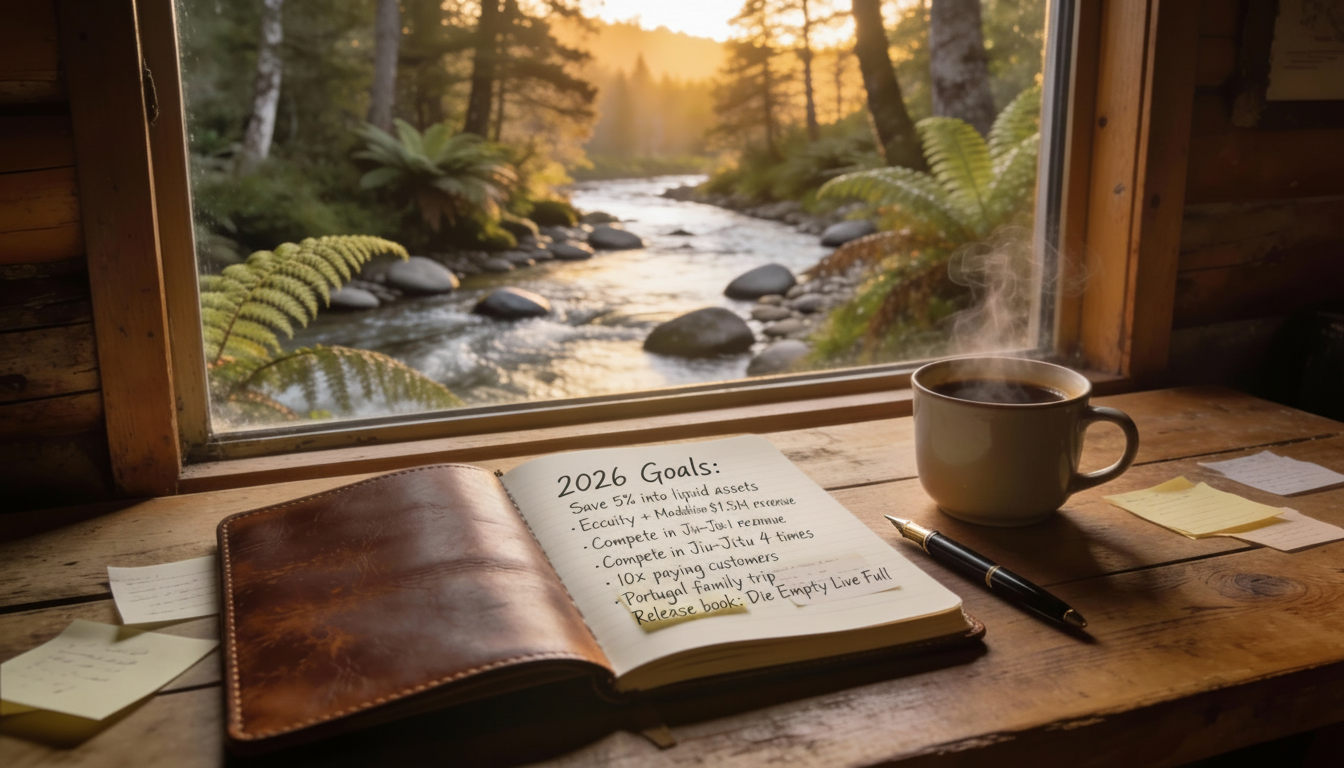

My 2026 12, 12, 12 Annual Goals

12 Months:

- Save 5% of my income into liquid assets

- Eccuity + Maddition revenue of $1,500,000

- Compete in Jiu-Jitsu 4 times

- 10x the number of paying customers using Eccuity

- Family trip to Portugal

- Release the book I have been working on

I don't really feel comfortable sharing the 12-day and 12-week goals in real-time. We like to talk about a lot of stuff, but on the micro level, we keep the execution internal.

In Conclusion

2025 was a huge success personally and as a business. I believe we were trending towards a blowout year, but given some setbacks at the end of the year I would conclude it was admirable, but setting us up for a very strong 2026.

I hope this inspires a few other people to set some goals and spend 2026 chasing them.

You can use our free net worth and planning tool for free today and forever.

References

All data in this memo has been fact-checked and sourced from market data providers, central banks, and financial institutions. Citations are embedded throughout the document corresponding to the following sources: Google OKR methodology, Naval Ravikant product philosophy, OpenAI funding rounds, precious metals markets, equity market performance, SaaS and consulting industry trends, New Zealand economic data, global inflation metrics, consumer stock performance, currency and metals markets, and Ray Dalio's portfolio theory.

LEGAL INFORMATION AND DISCLOSURES

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Maddition has no duty or obligation to update the information contained herein. Further, Maddition makes no representation, and it should not be assumed that past investment performance is an indication of future results. Moreover, wherever there is the profit potential there is also the possibility of loss.

This memorandum is being made available for informational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Maddition Limited. (“Maddition”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum (and previous referenced memoranda), including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Maddition.